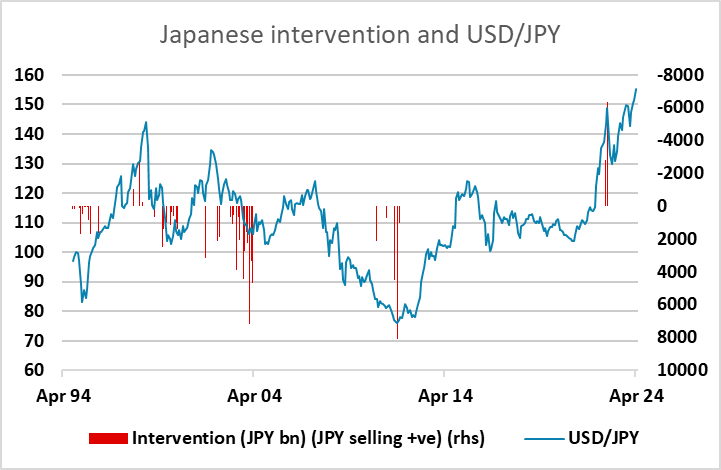

JPY flows: JPY weakness intensifies, intervention possible, but...

JPY weakness intensified overnight and increased the potential for intervention. This may be seen in the next few days, and the JPY does have potential to rally sharply given the huge real decline in recent years. But a turn higher in risk premia looks necessary to trigger a long term reversal of current weakenss.

More significant JPY losses have been seen overnight in spite of Japan chief cabinet secretary Hayashi joining the club with verbal intervention by saying rapid FX moves are undesirable and that he is ready for full response. The JPY has been making marginal new lows every day this week but has seen a bigger decline overnight, losing around 0.5%. The lack of intervenion so far may be emboldening the JPY bears, but we would expect some action from the Japanese authorities in the next few days unless the JPY recovers of its own accord.

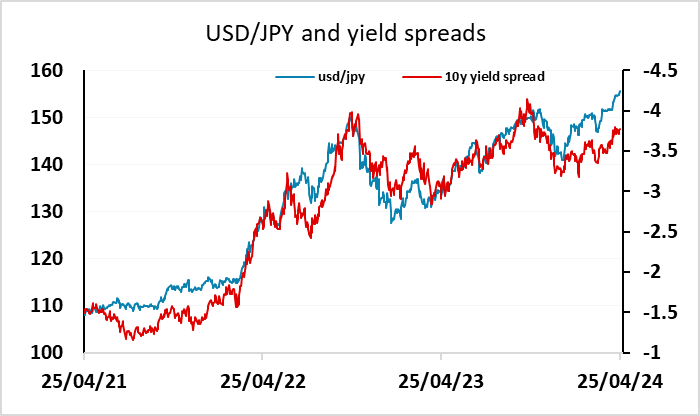

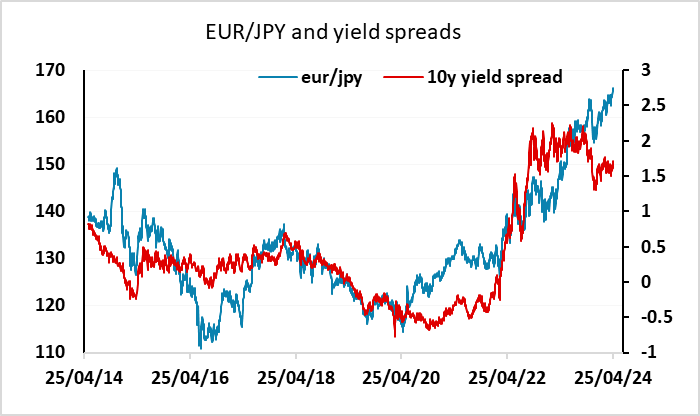

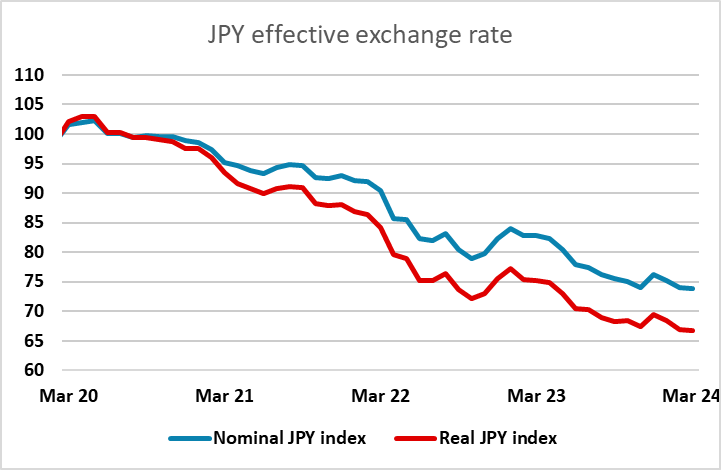

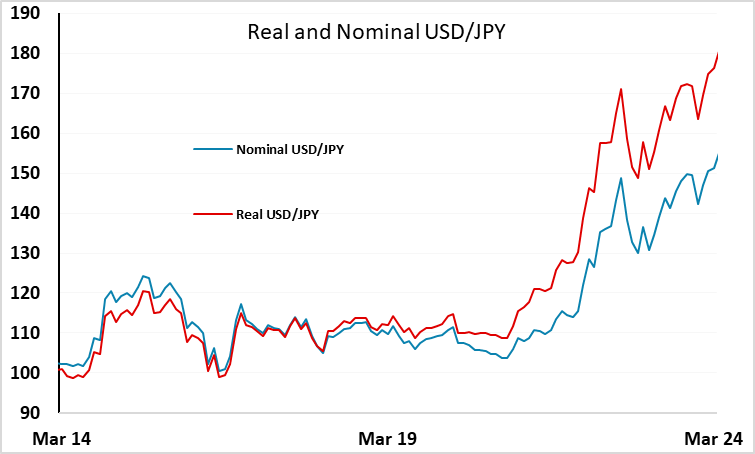

From a yield spread standpoint, there is no longer any support for further JPY weakness. This was always the prime factor seen as justifying the JPY’s decline since US and European yields started to rise back in late 2021. But the historic correlation with nominal yield spreads suggests USD/JPY should be trading nearer 145 than 155, while EUR/JPY should be close to 150. This is even without taking into account the fact that the JPY index has fallen 7% more in real terms than it has in nominal terms in the last 4 years, while USD/JPY has risen 18% more in real terms than in nominal terms. These real movements are more relevant in terms of long term value.

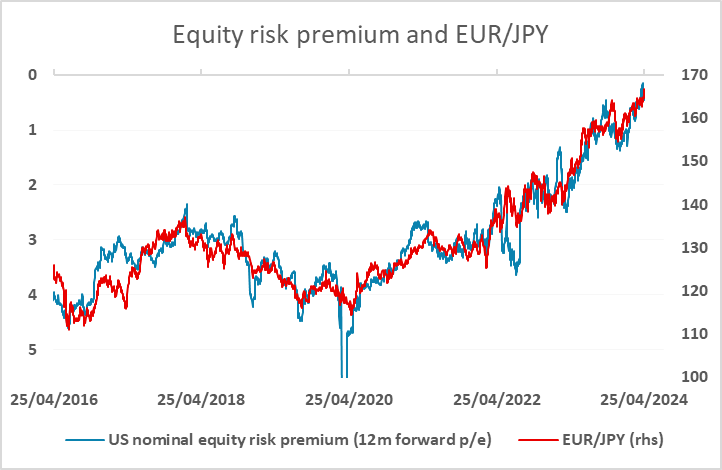

However, the main driver of JPY weakness continues to be the decline in equity risk premia, which continues to show a strong correlation with JPY weakness, particularly on the crosses. The fundamental justification for this is flimsy at best, but the correlation can’t be ignored. It has been particularly strong in the last 8 years, but has been evident since the GFC. The decline in equity risk premia is driven by the combination of rising yields and resilience in equities and projected earnings, and risk premia are now at similar low levels to those seen before the GFC. They are therefore likely to be close to a lower limit, but will probably require lower US yields if they are to decline.

The Japanese authorities will be aware of all these correlations. They will not want to take on the market and fail, but will be more inclined to intervene given the lack of yield spread support for JPY weakness. However, as long as there is little obvious negative economic impact from the weakness of the JPY, their incentive to intervene isn’t that clear. Most countries tend to be more concerned about a strong currency than a weak one, as long as the weak currency isn’t contributing to a cycle of inflation. At this stage, although Japanese inflation has risen, core inflation still looks to be under control and there is no current perceived need to tighten policy further. So the weakness of the JPY is not an enormous problem, especially as there seem to be no real complaints from trading partners.

Nevertheless, having warned continuously against excessive JPY weakness in recent weeks, some action looks necessary if the JPY continues to fall to avoid losing credibility. There is a BoJ meeting tomorrow, and the Japanese authorities may want to see the market reaction to that before deciding on their next course of action. No policy change is expected, but the market may react to the statement. Significant JPY weakness following the meeting may be may by intervention. Otherwise, a dawn raid on Monday may be a more likely tactical approach. Whatever happens on the intervention front, a rise in risk premia looks necessary longer term to turn the JPY higher. But the scope for JPY gains is greater than is obvious from the existing nominal correlations because of the big real decline in recent years.