FX Daily Strategy: N America, April 25th

US Q1 GDP the main focus

USD risks weighted to the downside

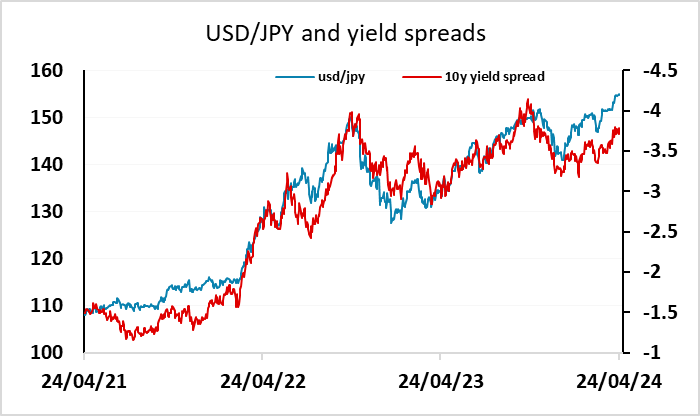

JPY intervention risk rising, but may wait until after Fridays BoJ meeting

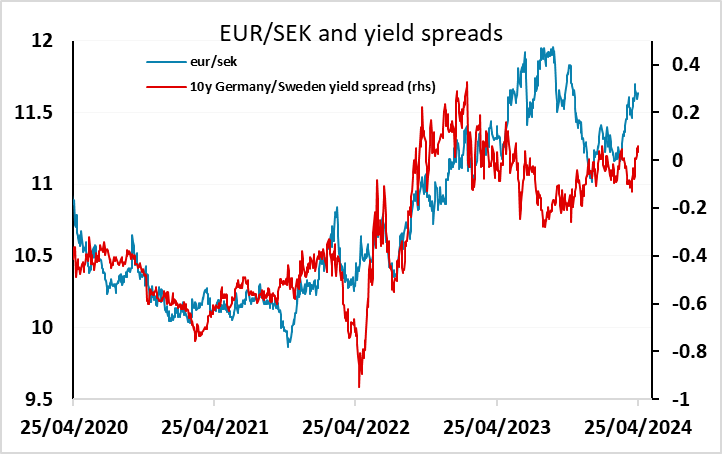

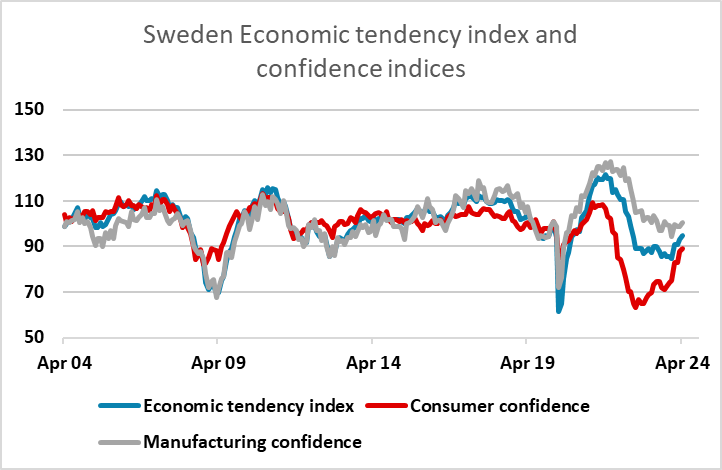

SEK has scope for gains after strong economic tendency survey

US Q1 GDP the main focus

USD risks weighted to the downside

JPY intervention risk rising, but may wait until after Fridays BoJ meeting

SEK has scope for gains after strong economic tendency survey

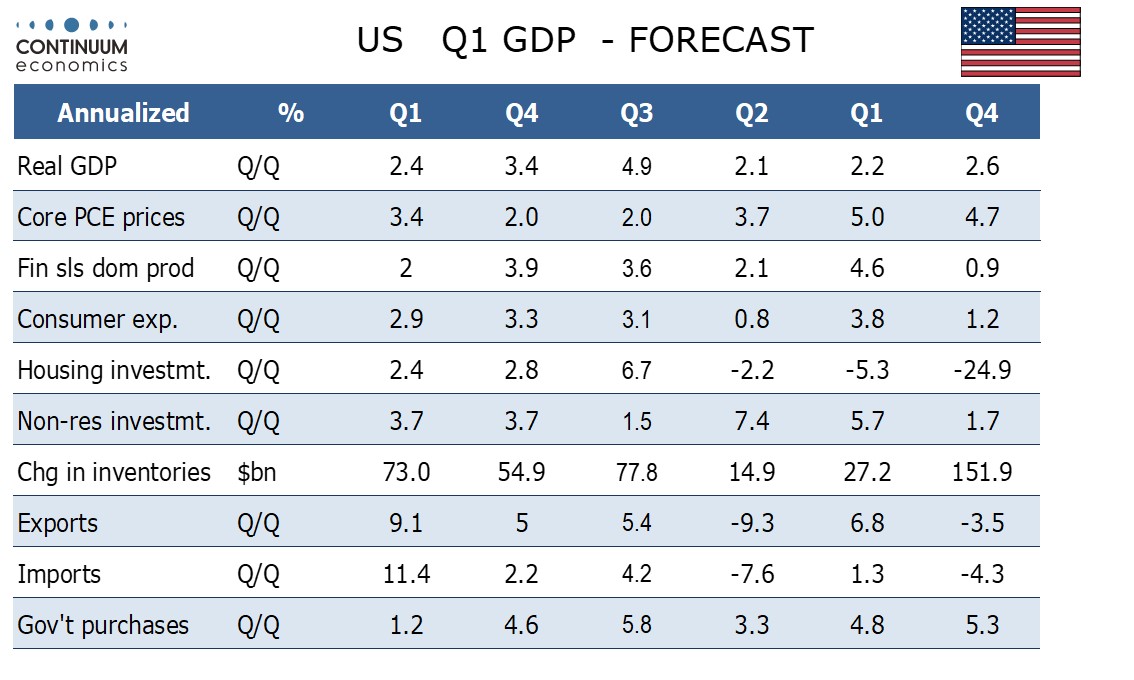

The main focus on Thursday will be the US Q1 GDP data. There will be as much interest in the price indices as in the growth numbers, although the growth numbers will perhaps be more in focus after the weaker than expected S&P PMI this week. We expect a 2.4% annualized increase in Q1 GDP, significantly slower than the second half of 2023 but slightly stronger than the first half and still a heathy pace of growth. We expect a pick up in the core PCE price index to 3.4% annualized after two straight quarters at 2.0%. Our numbers are in line with consensus, so probably wouldn’t have too much impact, but there is always potential for deviation from consensus in the first take on GDP.

The market moves in Q1 have shown that the market is more concerned with the inflation picture than the growth picture, as weaker growth and stronger inflation have led to a significant rise in yields, and seen the market move from pricing 6 rate cuts this year at the beginning of the year to less than 2 now. The less dovish market pricing has, however, been endorsed by several Fed speakers, even the normally dovish ones, so it still looks likely to require evidence of weaker inflation to have a significant market impact. In practice, the PCE price index is less likely to deviate from market consensus than the growth numbers, as we already have monthly data on the PCE price index for January and February and a good idea on March after the CPI data already released. Any deviation would nevertheless be important, given the market’s focus on inflation, but the odds are that the growth numbers are more likely to surprise. There may be more sensitivity to weaker rather than stronger Q1 data, as optimism around strong data would be moderated by the April PMIs suggesting a softer start to Q2. The sharp rise in US yields since the start of the year also looks a little overdone, and suggests risks weighted to the downside. Nevertheless, risks are still two way, even if there would probably be more reaction to weaker data.

The USD was modestly firmer on Wednesday in a quiet market , once again making new 34 year highs against the JPY and recovering a little of the ground lost on Tuesday against the riskier currencies. USD/JPY poked above 155 for the first time, and with USD/JPY above 155 and EUR/JPY above 165, the risks of intervention from the Japanese authorities is increasing, especially since the JPY weakness is not supported by movements in yield spreads. However, there is a BoJ meeting on Friday, which may affect the timing of any intervention decision. No action is expected from the BoJ, but the JPY may nevertheless react to the statement. The Japanese authorities may want to see this reaction and decide whether to act in the FX market with this information in hand. If they do decide intervention is appropriate, and early Monday morning raid next week might be the most likely timing.

The Swedish confidence numbers this morning have all been on the strong side of expectations, and the Swedish economic tendency survey which shows a reasonable long term correlation with GDP has recovered to its highest levels since August 2022 and is back to similar levels to those seen before the pandemic. This provides a fairly solid indication that the recession is over, and should provide some support for the SEK. EUR/SEK has traded higher than suggested by yield spread correlations in the last few weeks, and should now have potential to move back towards the 11 area which looks more consistent with current spreads. While the Eurozone also looks to be showing an improved growth performance, the SEK will tend to do better in periods where Europe is recovering, acting as something of a super-EUR.