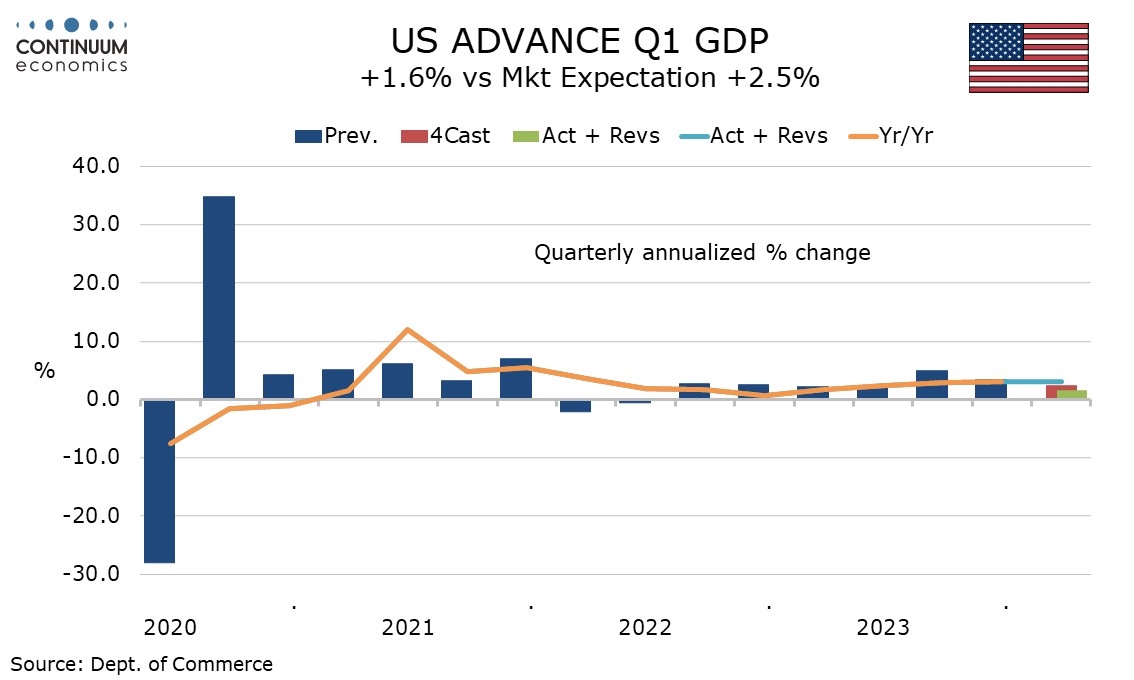

Q1 U.S. GDP Slows on Imports and Inventories, Core PCE Prices Stronger on the Quarter

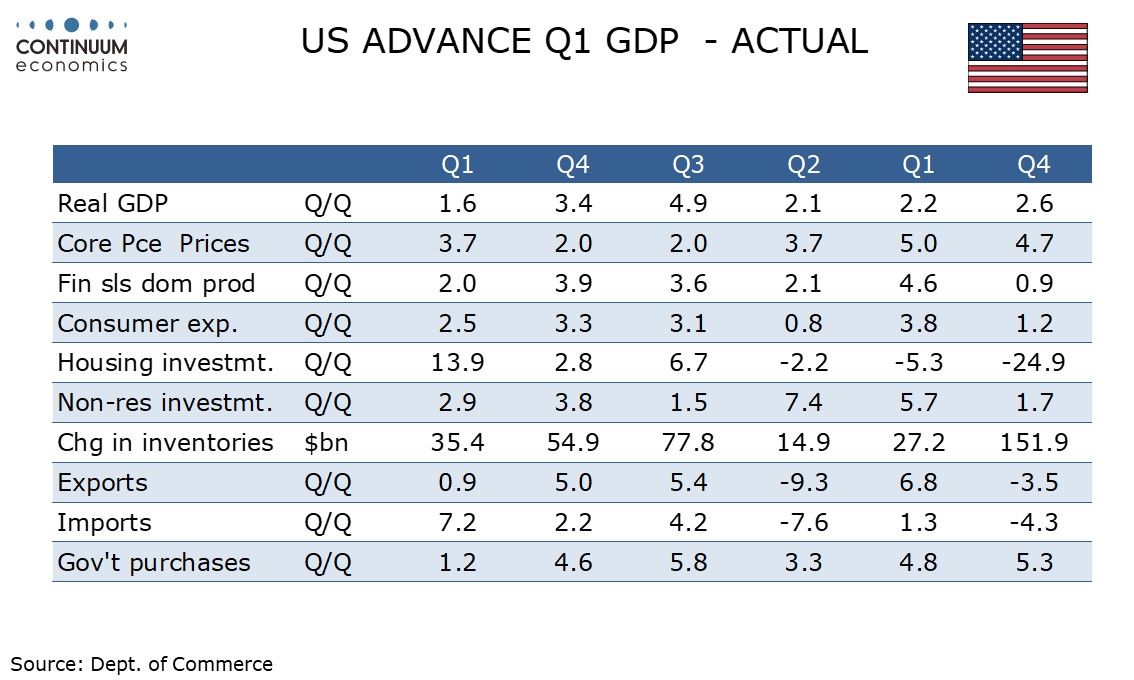

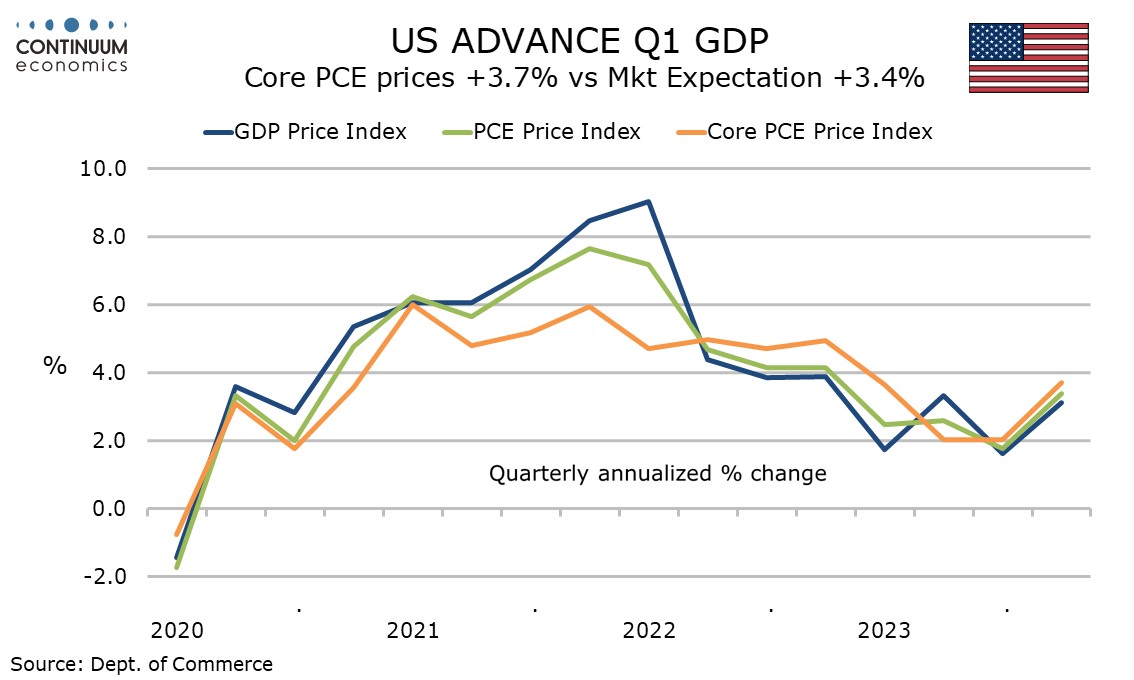

Q4 GDP has come in weaker than expected at 1.6% annualized but with a stronger than expected 3.7% annualized increase in the core PCE price index. Weaker inventories and stronger imports are the main reason for the GDP slowing so the data is not a clear signal of underlying weakness. Lower initial (207k from 212k) and continued (1781k from 1796k) claims show the labor market remains strong.

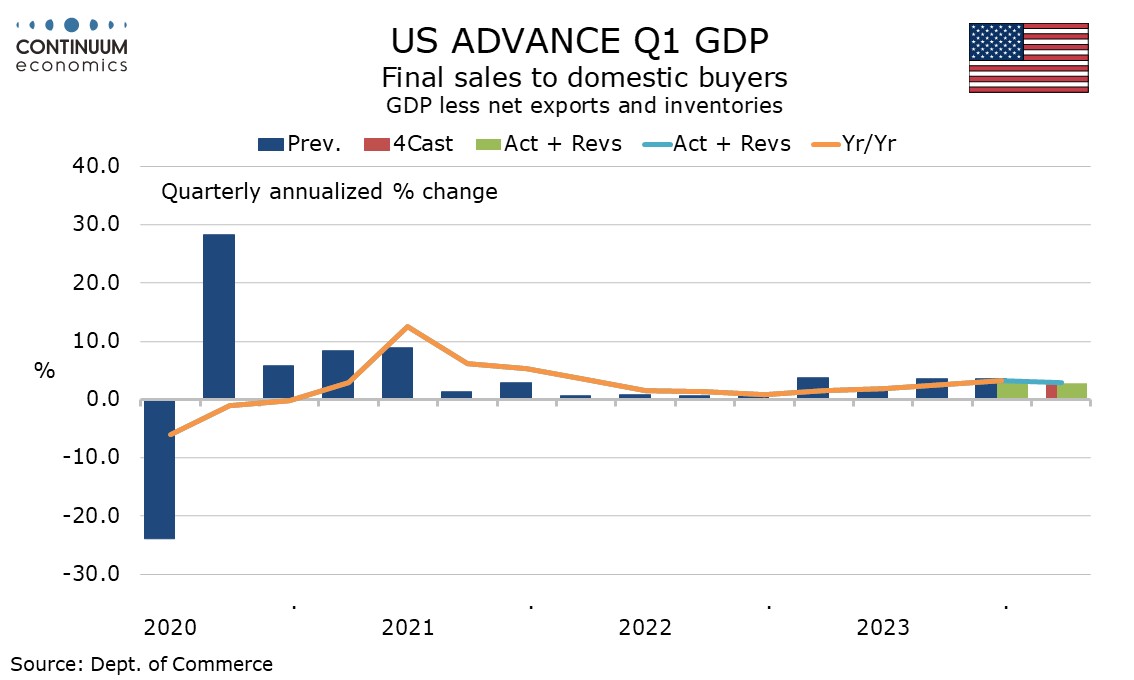

The GDP breakdown shows a 2.0% rise in final sales (GDP less inventories) and a 2.8% rise in final sales to domestic buyers (GDP less inventories and net exports) with net exports taking 0.86% from GDP and inventories taking off 0.35%. A wider advance March trade deficit and weaker than expected advance March retail and wholesale inventory data released alongside the GDP data is consistent with this.

Exports with a 0.9% increase were significantly slower than we expected and well behind a 7.2% rise in imports, which was also not as strong as we expected, but still left a significant negative from net exports.

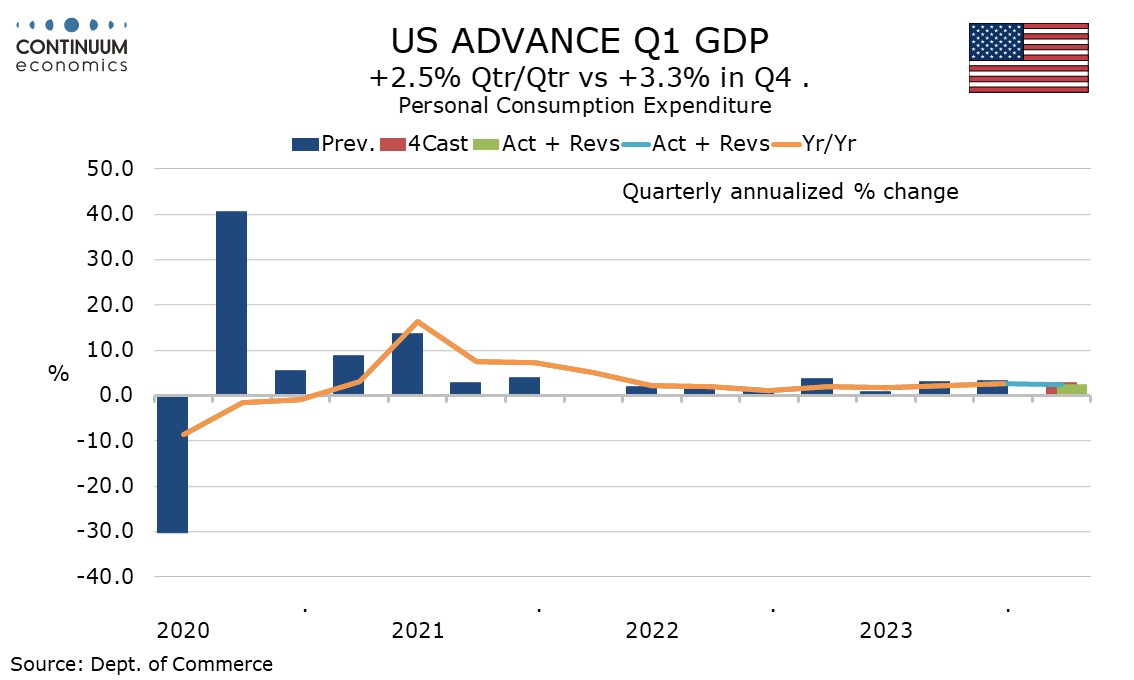

Consumer spending at 2.5% was slower than the previous two quarters showing strength in services at 4.0% but weakness in retail, though much of this was due to bad weather in January. Consumer spending continues to outpace real disposable income, which rose by 1.1%.

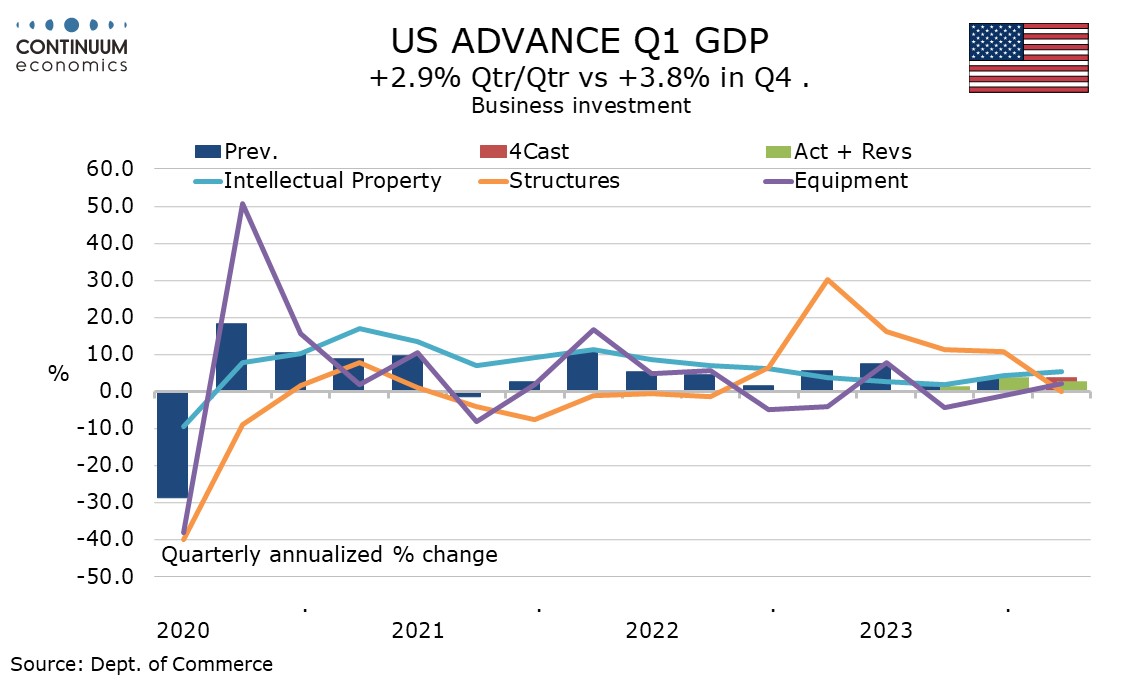

Business investment also rose at a moderate rise, of 2.9%, with structures slowing from recent strength but equipment showing its first increase in three quarters. Government at 1.2% saw a 7-quarter low with Federal slightly negative and State and Local up a modest 2.0%.

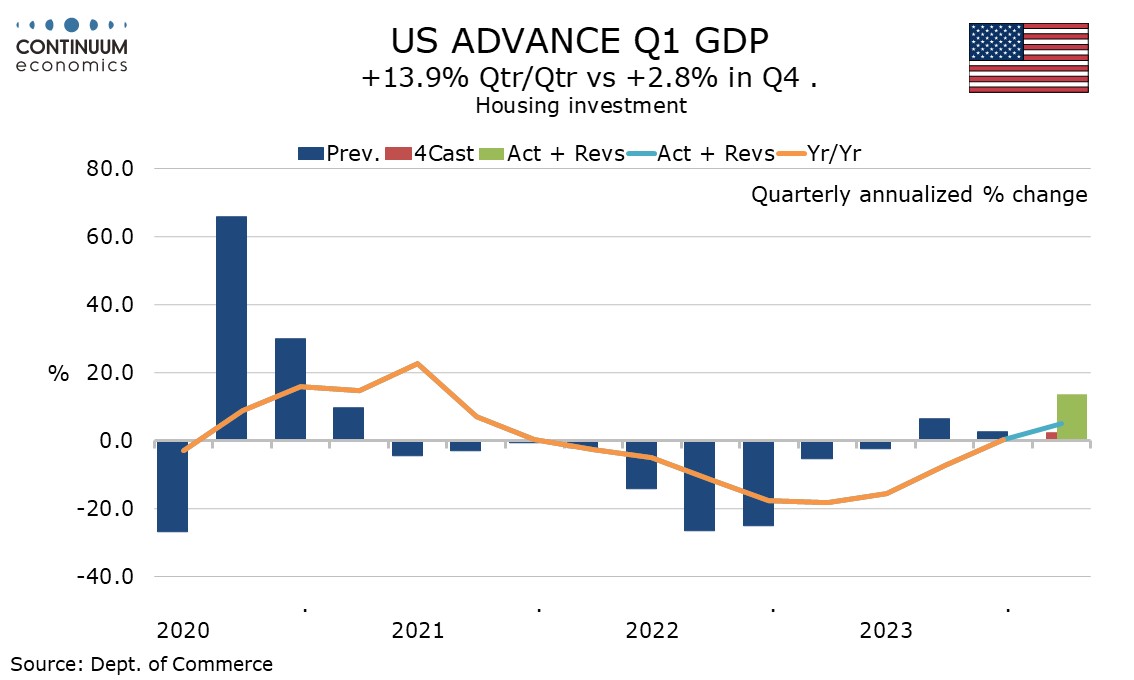

Housing was impressively strong with a 13.9% rise which will be hard to sustain given recent gains in mortgage rates.

The 3.7% rise in the core PCE price index suggests either an upside surprise in March data tomorrow or upward revisions in January and February. This follows two straight quarters on the 2.0% target and leaves yr/yr growth at 2.9%, still down from 3.2% in Q4 and the slowest since Q1 2021.

We suspect some of the Q1 strength in core PCE prices was seasonal not fully compensated by seasonal adjustments and the falling yr/yr data is consistent with that view. Still, inflation remains above target. The annualized gain in overall PCE prices was 3.4% and that for the overall GDP price index 3.1%.