Published: 2024-04-25T14:14:07.000Z

U.S. March Pending Home Sales bounce follows sharp February rise in Existing Home Sales

Senior Economist , North America

-

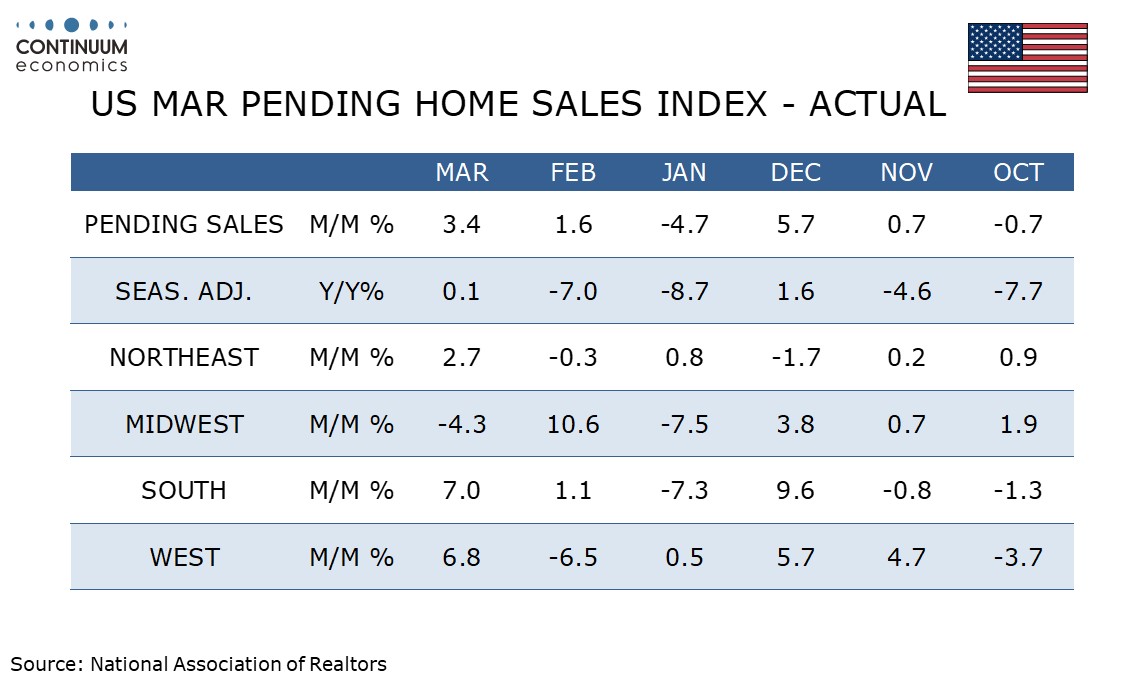

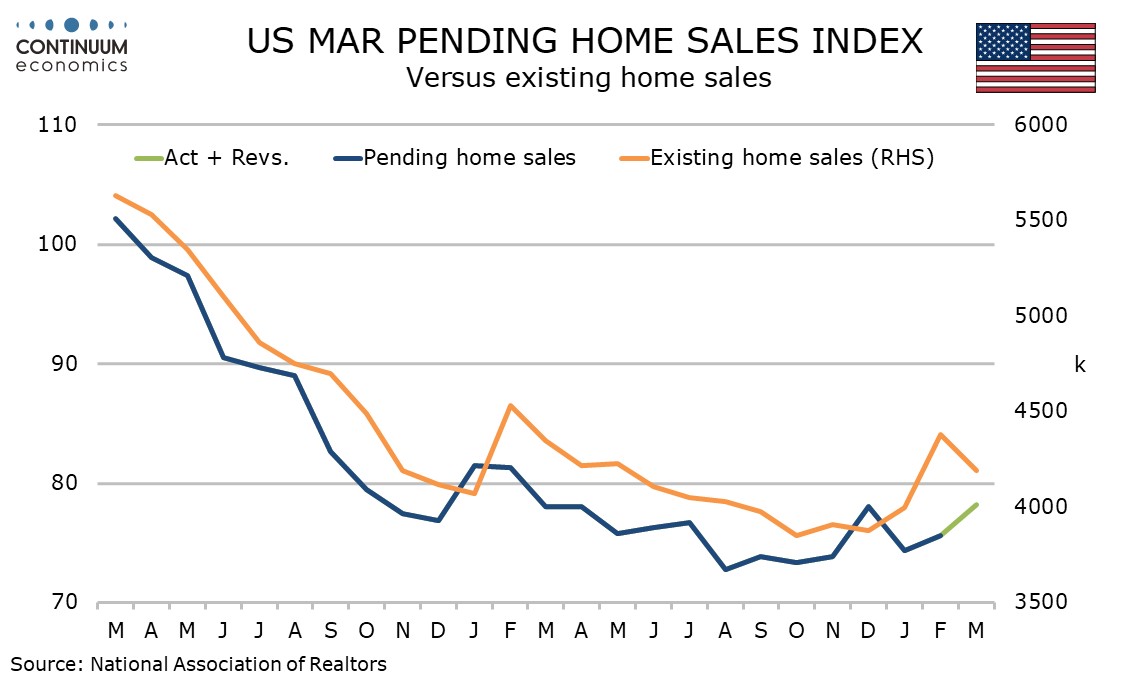

March has seen a stronger than expected 3.4% increase in pending home sales. Normally pending home sales lead existing home sales but in this case we appear to be seeing a catch up with strength in February existing home sales.

Housing investment was an area of strength in a Q1 GDP gain that overall fell short of expectations but the strength will be difficult to sustain given recent gains in mortgage rates.

2023 saw existing home sales peak after a strong February increase and we suspect the same will be the case in 2024.