FX Daily Strategy: APAC, April 26th

JPY may weaken if BoJ indicates no rush to tighten…

…potentially triggering FX intervention

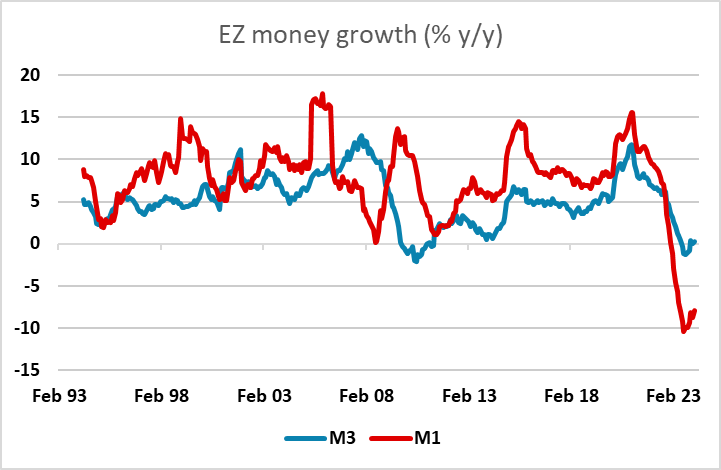

EUR/USD well supported but could suffer if Eurozone money data is weak

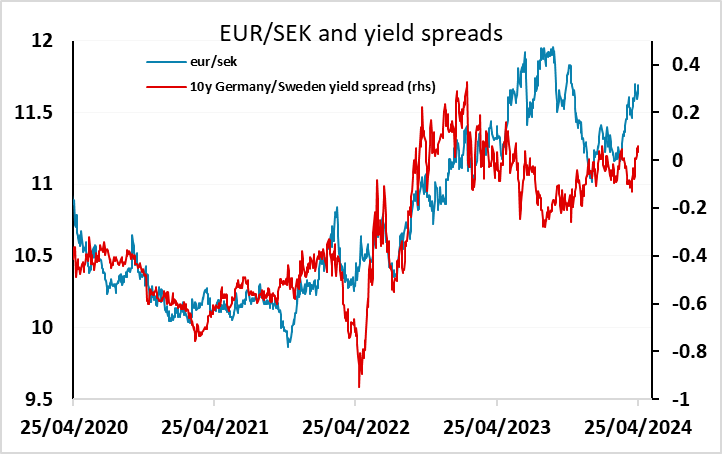

SEK has scope to recover after Thursday dip following strong Swedish data

JPY may weaken if BoJ indicates no rush to tighten…

…potentially triggering FX intervention

EUR/USD well supported but could suffer if Eurozone money data is weak

SEK has scope to recover after Thursday dip following strong Swedish data

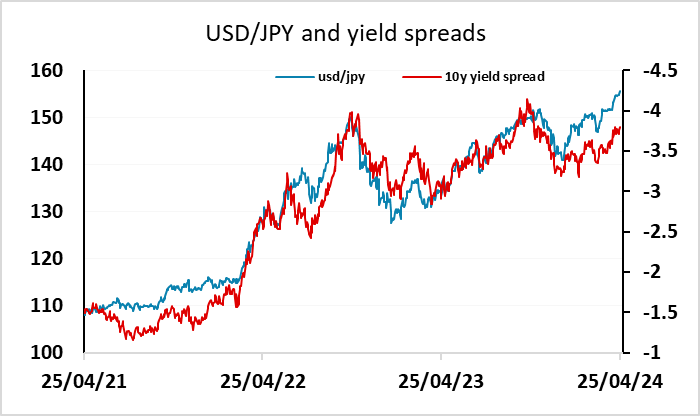

The BoJ meeting should be the highlight on Friday. It is preceded by the Tokyo CPI data for April, and this could have some impact on the tone of the statement if it is away from expectations, but there is no real chance of any change in policy at this meeting. We expect the BoJ to remain on hold and also signal that they are in no rush to tighten further. The BoJ has already moved the policy rate to 0% and officially removed YCC in March, citing trend inflation as being likely to achieve target. Looking forward, inflation is forecast to return below 2% by year end and does not support aggressive BoJ tightening. Such a stance could be expected to lead to further JPY weakening, as there are some market hopes of a more hawkish statement. This would increase the risk of FX intervention, but as long as the BoJ aren’t indicating that a weak JPY is a problem for the inflation outlook, we doubt intervention would be more than smoothing. However, stronger Tokyo CPI or an indication in the statement that the weakness of the JPY is likely to boost inflation above target could trigger a positive JPY reaction.

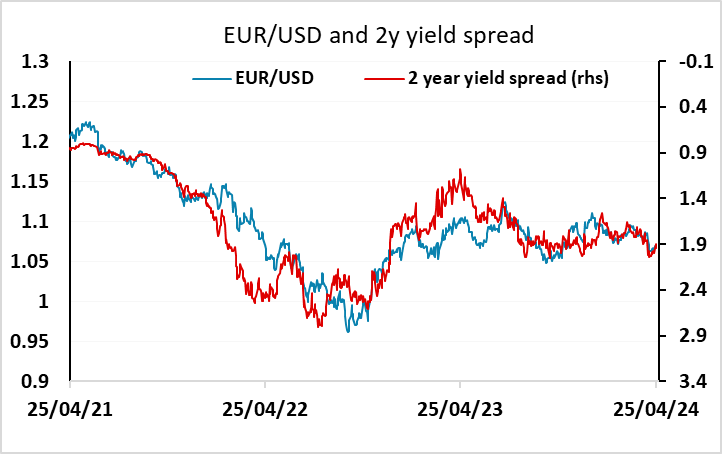

Elsewhere we have the March PCE deflator from the US, which now looks likely to come in at 0.4% following the 3.7% Q1 PCE deflator reported in the GDP numbers on Thursday. Alternatively, there could be an upward revision to the January or February data. Thursday saw a sharp bond market reaction to the stronger than expected deflator, with US yields rising around 7bps from 2 to 10 years. The first Fed rate cut is now not fully priced until November. But the USD impact was quite modest because European yields also rose and equities fell back in response, supporting the JPY and CHF, and in the end, the USD was little changed. While the rise in US yields need not be mirrored in European yields, particularly at the short end of the curve, rising European yields are easier to justify after the strong European PMIs this week. We would therefore expect the EUR to continue to be reasonably resilient to the higher US yield levels, with EUR/USD likely to hold close to 1.07.

However, Friday also sees Eurozone money and credit data, and this has shown significant weakness over the year, with both money growth and loan growth weakening significantly. The ECB bank lending survey specified that the reduction of the ECB’s monetary policy asset portfolio was at least partly responsible for this, resulting in a moderate tightening of terms and conditions and a negative effect on lending. More evidence of weakness in money and credit could therefore undermine the yield rise we saw in Thursday and push EUR/USD lower.

One FX move on Thursday that looked completely out of line with the news was the rise in EUR/SEK after a much stronger set of Swedish confidence numbers and the strongest economic tendency survey since August 1992. EUR/SEK already looks high relative to yield spreads, and the Swedish data suggests that the economy is emerging from the recent recession, which should prevent further yield spread moves against the SEK. Indeed, typically the Swedish economy is more volatile than the Eurozone so we may well see a relatively sharper Swedish recovery. This being the case, we would look for EUR/SEK to reverse strongly from the test above 11.70 seen on Thursday.