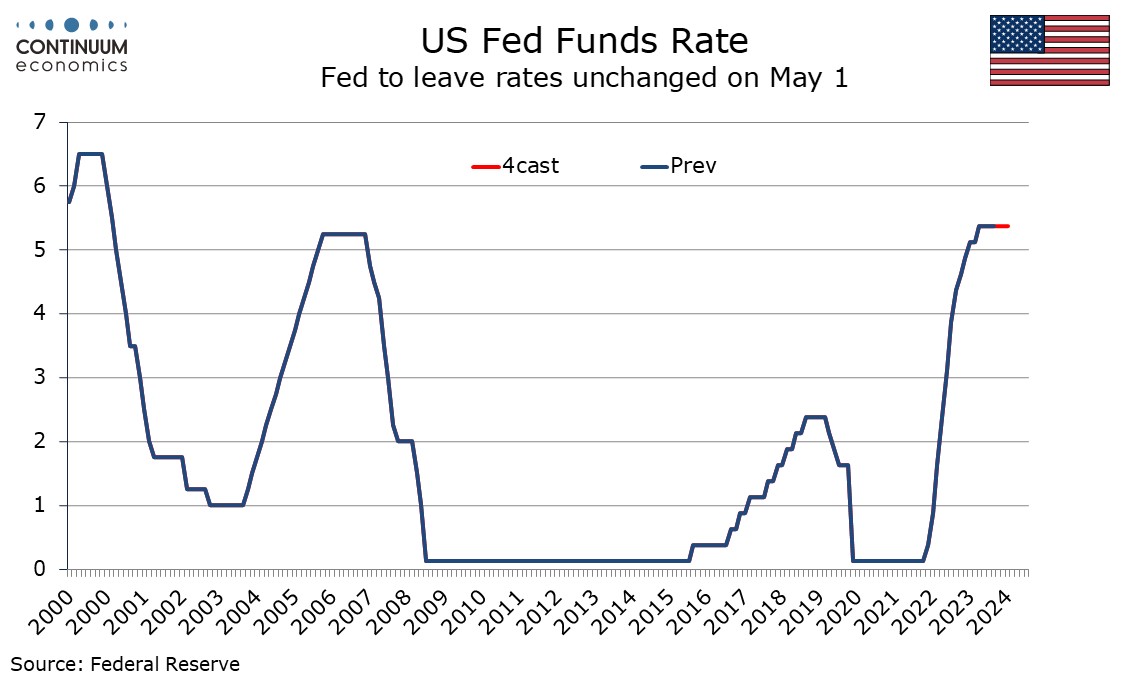

FOMC Preview For May 1: Signaling Concern on Inflation, Tapering Quantitative Tightening

Bottom Line: The FOMC meets on May 1 and rates look sure to remain at the current 5.25%-5.50% target range. The statement is likely to see some adjustments to reflect recent disappointment on inflation while repeating that more confidence on inflation moving towards target is needed before easing. It is also likely that tapering of Quantitative Tightening will be outlined at this meeting, but this should not be seen as a dovish policy signal.

The Statement

In the January and March statements the key wording was that “the Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2%”. This looks unlikely to be changed, though the FOMC is likely want to signal greater concern over inflation than was the case in March. A return to the language of late 2023, considering “any additional policy firming that may be appropriate” would be too hawkish a step, so the adjustments to the statement are likely to come elsewhere. In March the FOMC stated that “inflation has eased over the last year but remains elevated”. The reference to inflation easing is likely to be removed and replaced by language noting the stalling of progress or even renewed momentum. The FOMC may also consider removing or adjusting a sentence which stated “the Committee judges that the risks to achieving its inflation and employment goals are moving into a better balance”. The view that economic activity has been expanding at a solid pace is unlikely to change much despite the slower Q1 GDP gain, with details showing domestic demand remaining robust. That job gains have remained strong and unemployment has remained low needs no adjustment at all.

Powell’s Press Conference

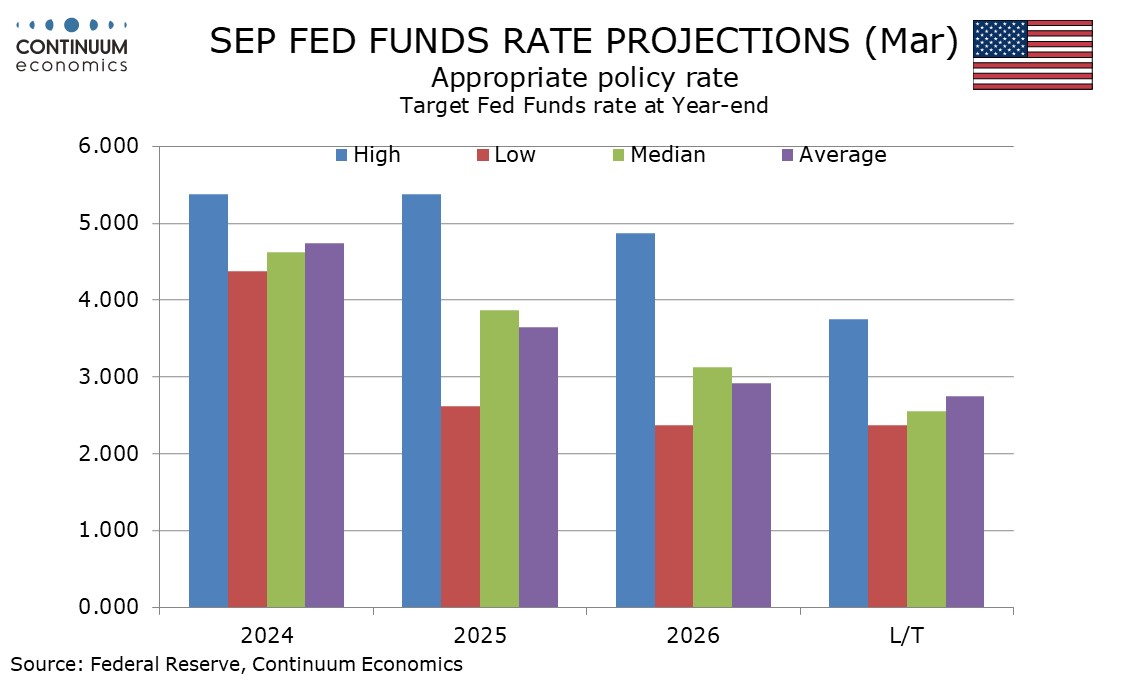

The dots will not be updated at this meeting, but Chairman Jerome Powell is likely to be cautious about giving a message consistent with the March dots that saw rates being eased this year. He is likely to stress that the dots are not a plan but dependent on the evolution of data, and recent data suggests that easing is not yet appropriate. The dots will next be updated on June 12. We will have seen non-farm payroll and CPI data for both April and May by then, with May CPI due on the morning of the decision. These releases are likely to determine how much, if any, easing in 2024 the dots project. March’s dots projected three 25bps easings in 2024 but only one participant needs to shift to leave the median at two. We expect that data will lose momentum sufficiently to allow easing later this year, and that is likely to be the view of the Fed too, but this is dependent on data where recent outcomes have raised uncertainty significantly.

Tapering Quantitative Tightening

At his March 20 press conference Powell stated that there was a general sense that it would be appropriate to slow the pace of balance sheet runoff fairly soon and the minutes of that meeting considered the issue in detail. After reviewing lessons from 2017-2019, participants broadly assessed a cautious approach to further runoff was appropriate with the vast majority favoring slowing the pace of runoff fairly soon. This did not mean that the balance sheet would ultimately shrink by less than it would otherwise. Participants generally favored reducing the monthly pace of runoff by roughly half from that seen currently while generally preferring to maintain the existing cap on agency MBS and adjust that on USTs. A plan along these line is likely to be announced, with tapering probably starting in June and the pace of balance sheet runoff likely to be cut in half by the end of the year. Announcing plans to taper the pace of Quantitative Tightening while delivering a somewhat hawkish statement on the policy outlook would help to prevent the plans, focused mainly on ensuring the smooth functioning of markets, as being misinterpreted as a dovish policy signal.