Published: 2024-04-26T15:32:59.000Z

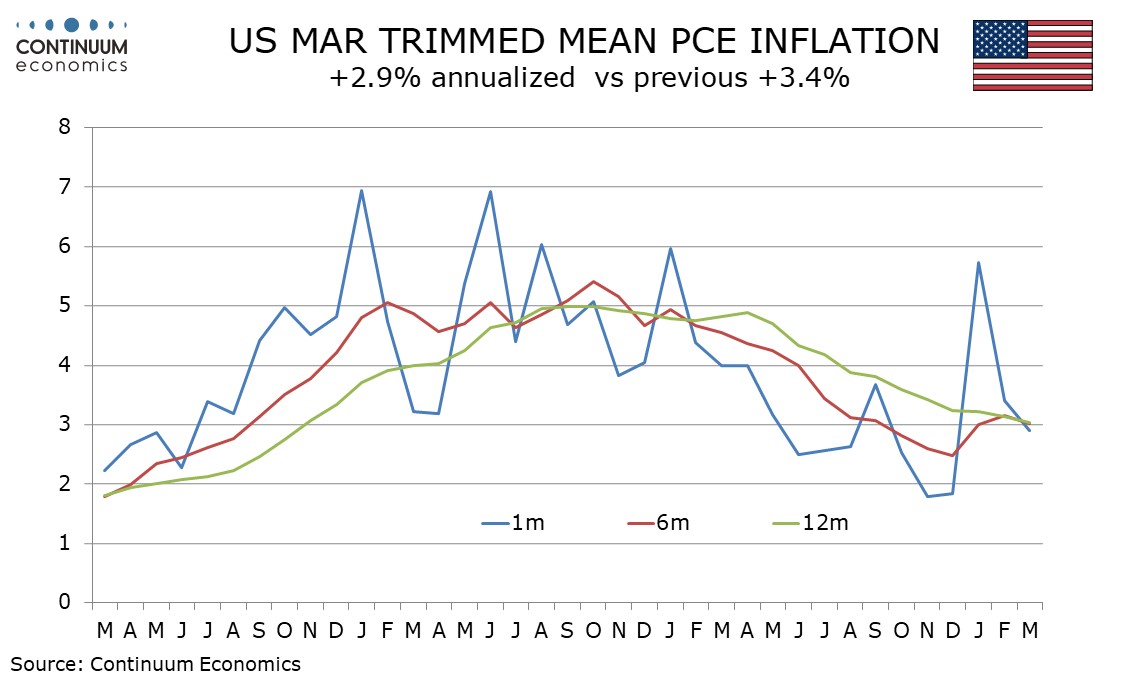

U.S. March Trimmed Mean PCE Price Index Slower at 2.9% Annualized

Senior Economist , North America

2

While March’s 0.3% Core PCE Price Index was a little firmer before rounding, and stronger than February data that was rounded up to 0.3%, the Dallas Fed’s Trimmed Mean PCE Price Index slowed to a 2.9% annualized pace from 3.4% in February.

Each month of Q1 is stronger than each month of Q4 but each month of Q1 2024 was softer than their respected outcomes of Q1 2023, meaning that yr/yr data continues to fall. We suspect there is some residual seasonality inflating data in Q1 while restraining that in Q4. The 6 month annualized pace of 3.02% is close to the yr/yr pace of 3.04%, and the monthly outcome for March..