FX Daily Strategy: Asia, May 9th

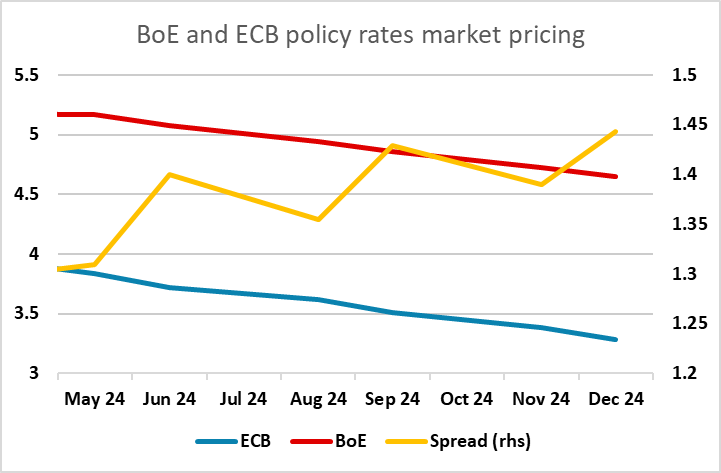

Some risk of more dovish BoE stance

EUR/GBP risks to the upside

JPY weakness looks unlikely to persist

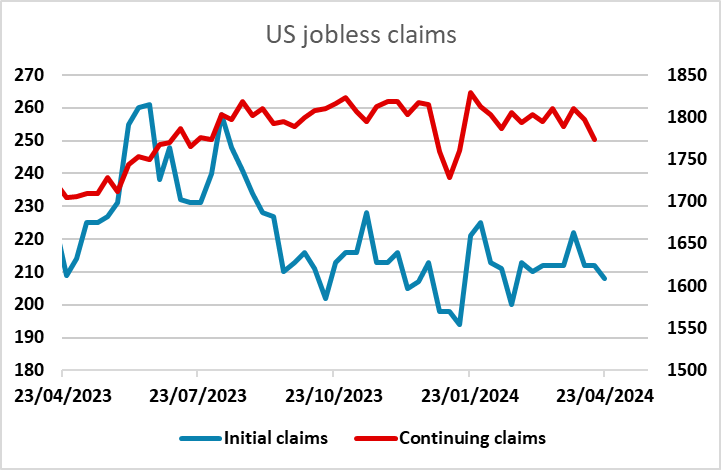

US jobless claims the US data focus

Some risk of more dovish BoE stance

EUR/GBP risks to the upside

JPY weakness looks unlikely to persist

US jobless claims the US data focus

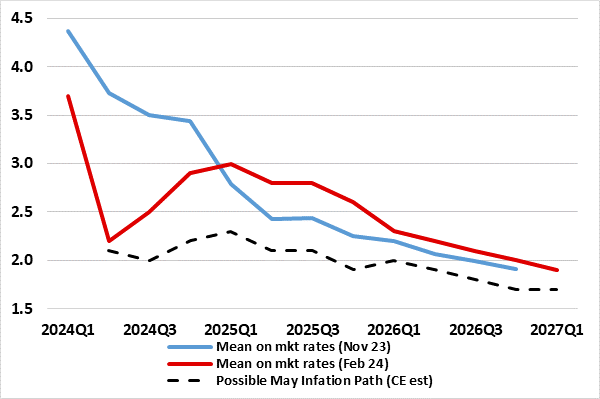

A Probable Softer Inflation Profile from the BoE?

A Probable Softer Inflation Profile from the BoE?

Source: BoE, CE

The Bank of England MPC meeting is the main item on the calendar today. In flagging no need to be dominated by Fed policy, we think that the BoE is moving towards rate cuts. But we do not see any move at the looming May 9 verdict, with Bank Rate again likely to remain at 5.25%. But the accompanying updated Monetary Policy Report (MPR) may show a much softer and more persistent near/below target inflation outlook, enough to make one or maybe two more MPC members vote for a cut even at this juncture. However, the rest of the MPC, not least the three hawks, will want to see the possibly vital April CPI data (due May 22) to assess the likelihood of a target undershoot and the extent to which persistent price pressures may have ebbed. Even given what we feel are somewhat better but exaggerated real economy signs now emerging, we remain of the view that disinflation (already evident even in falling services inflation) will continue. As a result, we still think the first 25 bp BoE cut may still arrive at the June 20 meeting and we look for around 75 bp of cuts this year and even more in 2025.

As it stands, the market isn’t pricing any chance of a rate cut today, but June is priced at slightly less than a 50-50 chance. The signal from this meeting is therefore crucial. Of course, given that the April CPI data isn’t due until later this month, today’s statement probably won’t be conclusive. But it should signal whether the April data needs to be weak to justify a cut, or whether it needs to be strong to dissuade the MPC from cutting. If there is more than one vote for a cut this month it would be a strong signal that the Bank is primed to cut in June. If we stay at just one vote for a cut, the language or the forecasts of the MPR will need to be clearly dovish to move the dial so that June id seen as a probable rather than a possible move. But we do see the risks as being towards more dovish outcome, and EUR/GBP risks should consequently be on the upside.

Otherwise, the Japanese cash earnings data for March may be the most significant data release. In practice the BoJ are more concerned with the wage deals for the coming year, so the March data probably won’t have a huge impact. However, weak numbers could extend the softer JPY tone that we have seen so far this week. If so, it could potentially trigger BoJ intervention once again. The USD/JPY gains we have seen have been corrective, but it’s hard to see them as being caused by the squaring of short USD positions given that the USD/JPY decline happened so rapidly and the CFTC data shows net JPY speculative positioning was still very short as of last Tuesday. The BoJ may want to wait until the technical target at 157 has been hit before coming in again, but with US yields not supporting the latest JPY decline, and we see little reason for further JPY losses.

Otherwise, we have the usual US jobless claims numbers, which perhaps take on a little more significance after the slightly weaker US employment report and the softer PMI and ISM numbers in the last week. So far there has been no real evidence of significant softening in the labour market, but a rise in jobless claims on top of the other data could trigger more significant USD losses.